Research notes and launch updates.

From blind enthusiasm to interrogation.

The AI trade is no longer moving in a straight line. Since everyone is an AI company now — but not everyone is good at AI — confidence in some AI-linked stocks has started to wobble, and share prices have followed. That does not mean the AI story is broken. It means the market is moving from blind enthusiasm to interrogation.

Following months of unconstrained spending and growth, with valuations and investment announcements never seen at this scale, the hype faces its first tests — investors starting to realise that perhaps not everyone will be a winner, and not all of the investments will lead to positive returns.

Our view is that this is a healthy but important shift — investors are no longer willing to underwrite every AI narrative at any price. The next phase of the market will be less forgiving, but probably more useful: real AI businesses should become easier to separate from AI-labelled optimism, and spending has to have at least some evidence of sense behind it.

Sources: Meta cloud business · Blackstone × Google TPU cloud · Brookfield $100B AI programme · Related Digital / Oracle $16B data centre

Macro

The macro backdrop, theme by theme — and our read.

| Factor / Theme | Our read |

|---|---|

| The US labour market is cooling | Giving markets permission to think central banks may be less aggressive, but weaker hiring is not automatically bullish if it starts to affect demand, confidence and earnings. |

| Rates | The key variable underneath almost everything: AI valuations, IPO appetite, M&A financing, private equity exits and the willingness of investors to underwrite long-duration growth. Understandably, the US President will continue to try and have the Fed keep rates at (artificially) low levels. It remains to be seen how this unfolds, and what reactions the global banking community will have once there is clarity. |

| AI Capex | Moving from an equity-market story to a balance-sheet and credit-market story. The question is no longer just "who wins AI?", but "who funds it, at what cost, and with what payback period?" |

| The IPO window | Looking more open, but to a select group. Landmark names can list; average companies still need cleaner numbers, stronger growth, and a more credible path to profitability. SoftBank is trying to unload / lighten quite a lot of its exposure (OpenAI, Rozo, SB Energy). |

| Public markets | Still rewarding scale, scarcity and narrative, but the next correction will probably punish companies where the narrative has moved faster than cash flow. |

Public markets

M&A

The message from markets is not that risk appetite has fully returned. Capital is available for assets that can tell a story around scale, strategic relevance and long-term demand. M&A is being driven by large, board-level moves. AI is being driven by infrastructure intensity. IPOs are being driven by scarcity and, to some extent, brand value. That is investable, but it is not risk-free.

Staying Diligent

Things we are watching next:

- Fed minutes The key market event is the release of the June Fed minutes. After cooling labour data and recent volatility in tech, investors will be looking for any signal on whether the Fed is still leaning hawkish or becoming more cautious.

- AI equities AI-linked equities remain the market's pressure point. Watch whether the recent weakness in semiconductors and AI infrastructure names becomes a short-term reset or the start of a broader rotation away from the most crowded part of the market.

- Earnings Delta Air Lines and PepsiCo start the early earnings cycle, and they could give a real-time read on consumers, pricing power, travel demand and whether earnings can support equity valuations.

- Central banks The ECB minutes and Bank of England financial-stability commentary will all matter for rates, currencies and risk appetite. The key question is whether global central banks are still fighting inflation, or starting to worry more about growth.

- Europe data German and French trade and industrial data will be worth watching. Europe remains a valuation-sensitive market, and any sign of weaker industrial activity could pressure cyclicals, exporters and M&A confidence.

- Oil Oil has calmed down from recent war-driven volatility, but the market remains vulnerable to OPEC+ signalling, Middle East developments and any renewed disruption to supply or shipping routes.

- NATO summit The NATO summit could matter for European defence, infrastructure and fiscal policy. If governments move from political commitments to real budget allocations, defence-linked equities and supply-chain names will stay in focus.

Unhedged Commentary

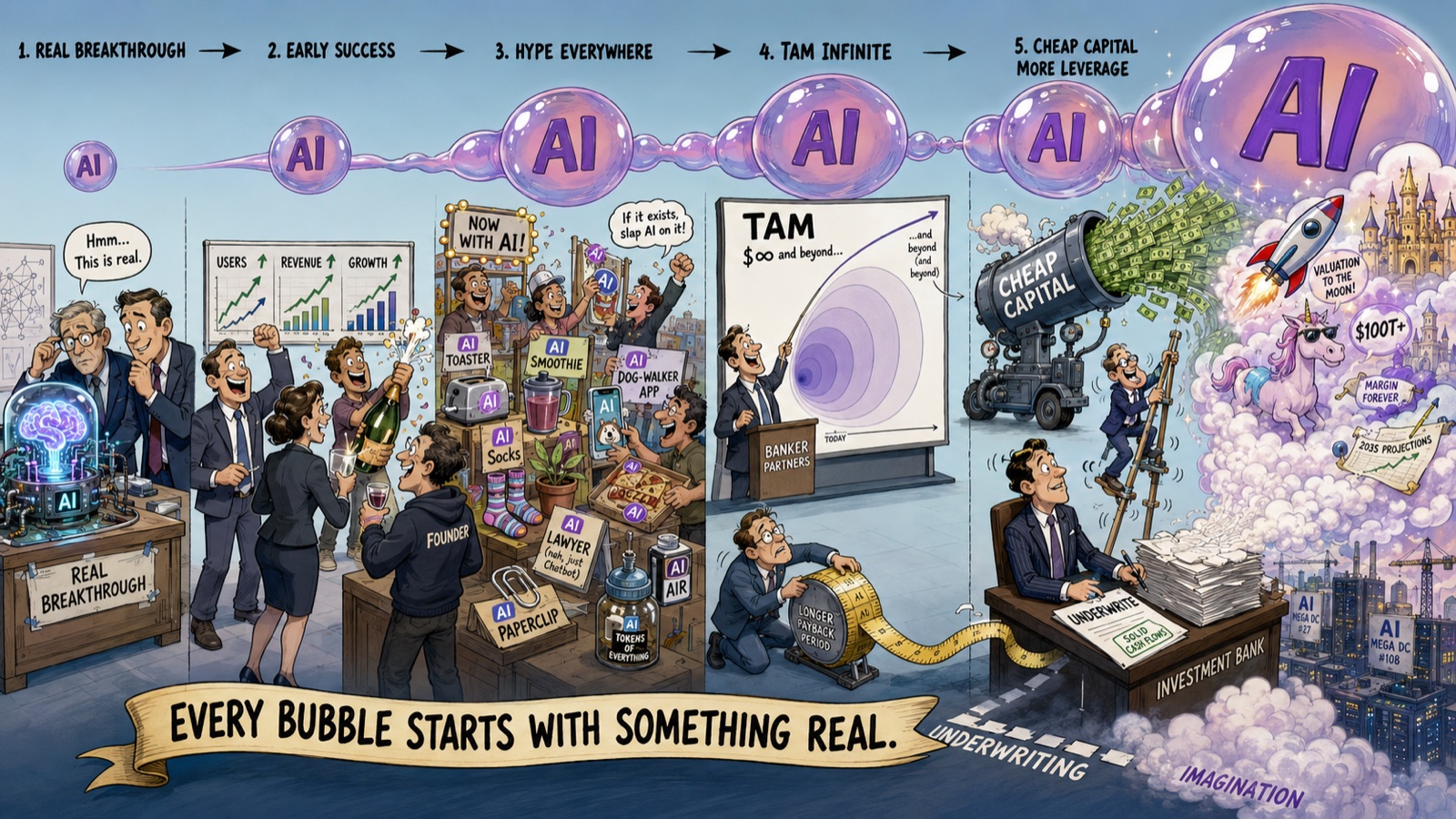

Every bubble starts with something real

The lazy version of market commentary is to call everything that grows quickly a bubble. The equally lazy version is to say that because a technology is real, valuations must be justified. History is less comfortable than either view.

Railways were real. The internet was real. Mobile was real. Cloud was real. AI is real. In almost every major technology cycle, the underlying innovation genuinely changed the economy. The problem was not that investors believed in the wrong technology. The problem was that they believed in the right technology too early, at the wrong price, with too much leverage, and with too little discrimination between winners, suppliers, tourists and storytellers.

The pattern is familiar.

- A real breakthrough appears.

- A few early companies show extraordinary growth. Smart, industry-focused investors and funds identify the theme and move in, with great success (which they are happy to be loud about).

- Every company starts attaching itself to the theme.

- TAM slides get bigger.

- Payback periods get longer.

- Capital gets cheaper.

- Infrastructure gets overbuilt.

The line between underwriting and imagination starts to disappear.

AI has many of the same ingredients. The technology is transformative, but the market is already capitalising future productivity gains before many companies have proved where those gains turn into revenue, margins or durable competitive advantage. Even now, there is a perception that between all of the deals happening, the same productivity gain has been "underwritten" to justify the returns for several deals at once. We've levered up on an imaginary number that only exists because someone on the Bain team had to make an assumption for their client's M&A diligence slides.

The winners will not be the companies with the loudest AI positioning. They will be the ones that solve painful, repeatable, high-value problems where the customer can see the productivity gain and trust the output — companies able to do this while keeping at least line-of-sight with economics and unit cost.

That is where we think the next serious software companies will be built: not generic AI wrappers, but workflow-specific systems that turn messy information into reliable decisions. We're already seeing it in some industries — the second wave of AI companies, sitting between the wrappers and the research labs.

Our view: The AI correction, when it comes, will not mean AI failed. It will mean the market funded too much, too fast, in too many places, before the cash flows caught up. As it always does.

In Other News

The old guard still has something to say

One of the best stories of the World Cup is not just the emergence of new stars, but the refusal of the old guard to disappear quietly. Messi and Ronaldo are no longer just footballers. They are case studies in obsession, adaptation and longevity.

At this stage of their careers, neither is operating on youth, novelty or physical dominance alone. They are competing on decision-making, preparation, timing, emotional control and an almost irrational level of professional commitment. There is something deeply impressive about that.

The easy narrative in sport, business and markets is that everything belongs to the new generation. Sometimes it does. But longevity is underrated. Staying relevant after everyone has already written your ending requires a different kind of talent.

In startups, investing and sport, the same rule often applies: early brilliance gets attention, but repeated reinvention is what creates legacy.

The Thinking Corner

If AI is both a real technology shift and a potential valuation bubble, how should investors separate companies building durable workflow value from companies simply borrowing the language of the cycle?

Latest from the team

Market commentary and field notes from the team, on The Felix View.

The securities referenced do not represent buy or sell recommendations. These notes describe corporate events and possible catalysts only. Figures are sourced from public filings, company presentations and market data; every claim links to its source. Prepared for institutional research use.