Research notes and launch updates.

Time to walk the walk.

Companies have been making promises and issuing positive news over the past months, and markets have been pricing these stories. Now that it's quarterly earnings season, we get to take a look at the evidence — while we still can, at least. One story that has gotten little attention (apparently there are other topics people would rather talk about) is the SEC's proposal to move away from quarterly earnings reporting, which more and more companies are backing.

AI capex, consumer resilience, bank deal pipelines and corporate margins are all moving into the same frame: proof. It is no longer enough to say demand is strong, AI spending will pay back, or the consumer is holding up. Investors need to see it in revenue, margins, guidance and cash flow, now more than ever, because not all parts of the trade are holding up as well as they did some time ago.

Remember the KOSPI? After reaching all-time highs in late June, it has since fallen 25% (as of the time of writing).

Our view is that this is a useful reset. The market is not necessarily turning risk-off, but it is becoming less tolerant of lazy optimism. The companies that can show real demand, pricing power and operating discipline should keep attracting capital. The companies relying mainly on narrative may find the next few weeks less forgiving.

Macro

The macro backdrop, theme by theme — and our read.

| Factor / Theme | Our read |

|---|---|

| Oil / Iran risk | Oil has not disappeared as a macro risk. Any renewed pressure on supply or shipping routes can quickly feed back into inflation expectations, central-bank pricing and consumer margins. The latest U.S. strikes are a reminder that geopolitical risk can move from background noise to market input very quickly. |

| NATO / Defence spending | The emotional read is instability. The fundamental read is higher European defence spending, more focus on capability, and a broader definition of national and European security. |

| Inflation | US CPI and PPI are the cleanest macro tests this week. The market can live with slower growth if inflation is cooling. It becomes harder if inflation stays sticky while earnings are being tested. The Fed's latest report already flagged stepped-up inflation pressure from tariffs, the Iran war and AI-related investment. |

| AI capex | AI investment is still supporting growth, but the market is starting to ask whether the spending is productive, inflationary, or both. The next phase is about showing credible returns on capital. |

| U.S. equities | The market is not ignoring risk, but it is still willing to look through it when earnings and AI fundamentals remain supportive. The next test is whether results can justify the valuation move. |

| Global M&A pulse | The deal market is reopening, but it is not indiscriminate. The strongest activity is where buyers can point to scale, strategic necessity, defence exposure, AI infrastructure relevance, healthcare durability or portfolio simplification. |

Public markets

M&A

Staying Diligent

Things we are watching this week: 13-17 July 2026.

- U.S. CPI The week's cleanest macro test. A soft print gives markets room to keep believing in rate relief. A hot print makes the "earnings season is the lie detector" theme even sharper, because valuations would need to survive both higher prices and less policy flexibility.

- U.S. PPI Producer prices matter because they show whether inflation pressure is still sitting inside corporate cost bases. If input costs stay sticky, margins become harder to defend.

- Retail sales The consumer is still the market's favourite argument for resilience. Retail sales will help show whether spending is genuinely healthy, or whether households are simply paying more for the same basket.

- Big U.S. banks JPMorgan, Goldman Sachs, Citi, Bank of America, Wells Fargo and Morgan Stanley will give the first proper read on trading, investment banking, credit quality and deal pipelines. If bank commentary is strong, the M&A recovery becomes easier to believe.

- TSMC and ASML The most important AI infrastructure read-throughs of the week. Investors will look for evidence that semiconductor demand remains strong enough to justify the capex cycle, not just the narrative around it.

- BlackRock Watch flows. BlackRock is a useful window into where capital is moving: equities, fixed income, private markets, cash or alternatives. In a market debating risk appetite, flows matter.

- Fed testimony Markets will listen for any shift in tone on inflation, labour-market cooling and growth. The Beige Book should also give a more grounded view of regional business conditions than the headline index moves.

- China data Important for global demand, industrial sentiment and AI hardware supply chains. Any weakness would matter for cyclicals, exporters and the wider global growth narrative.

- Oil and Iran Geopolitical risk has not disappeared. The renewed tension around Iran could have significant impacts on oil supply or shipping routes, with implications for inflation expectations and central-bank pricing.

- Mansion House speech Worth watching for UK financial services, especially if policy support for AI adoption, capital markets reform or growth investment becomes more concrete.

- AI equity breadth The market needs to show whether AI strength is broadening or narrowing. If only the highest-quality names hold up while second-tier AI beneficiaries weaken, the market is becoming more selective rather than simply more bullish.

Unhedged Commentary

Fear is not a framework

The NATO summit in Ankara gave markets mixed signals: on one hand, noise and uncertainty; on the other, stronger fundamentals for security spending.

There was plenty to worry about on the surface. Trump arrived with familiar pressure on European defence spending. Allies were anxious about U.S. reliability. Ukraine remained central. Russia was watching. Turkey, as host, sat at the intersection of NATO politics, Black Sea security, the Middle East and its own complicated relationship with the West.

It would be easy to read the whole thing emotionally: NATO is divided, America is unpredictable, Europe is exposed, Russia is waiting, markets should be nervous.

The more useful read is underneath the noise. NATO did not collapse. Article 5 was reaffirmed. Ukraine received further political and military support. Europe is still moving towards higher defence spending. The defence-industrial base is becoming a larger policy priority. Turkey's role inside the alliance remains complicated, but strategically important. The direction of travel is towards higher security spending.

That matters for investors because fear and fundamentals often move at different speeds. Fear prices the headline. Fundamentals price the follow-through.

The headline could be instability. The fundamental is that Europe is structurally underinvested in defence, logistics, cyber, air defence, munitions, energy security and critical infrastructure. The headline is Trump saying something unpredictable. The fundamental is that European governments are being pushed, politically and strategically, towards higher defence capability regardless of who sits in the White House.

That does not mean every defence stock is cheap. It does not mean every budget promise becomes real spending. It does not mean Europe can rebuild industrial capacity overnight. There will be procurement delays, political pushback, fiscal pressure and plenty of waste.

But the investment question is not whether the NATO meeting felt calm. The investment question is whether the underlying direction changed.

Our view: the meeting confirmed a messy but durable shift. Europe is being forced to take security more seriously. Defence spending is becoming less discretionary. Supply chains, energy systems, cyber resilience and infrastructure are becoming part of national security, not just public policy. That is the part worth underwriting.

In Other News

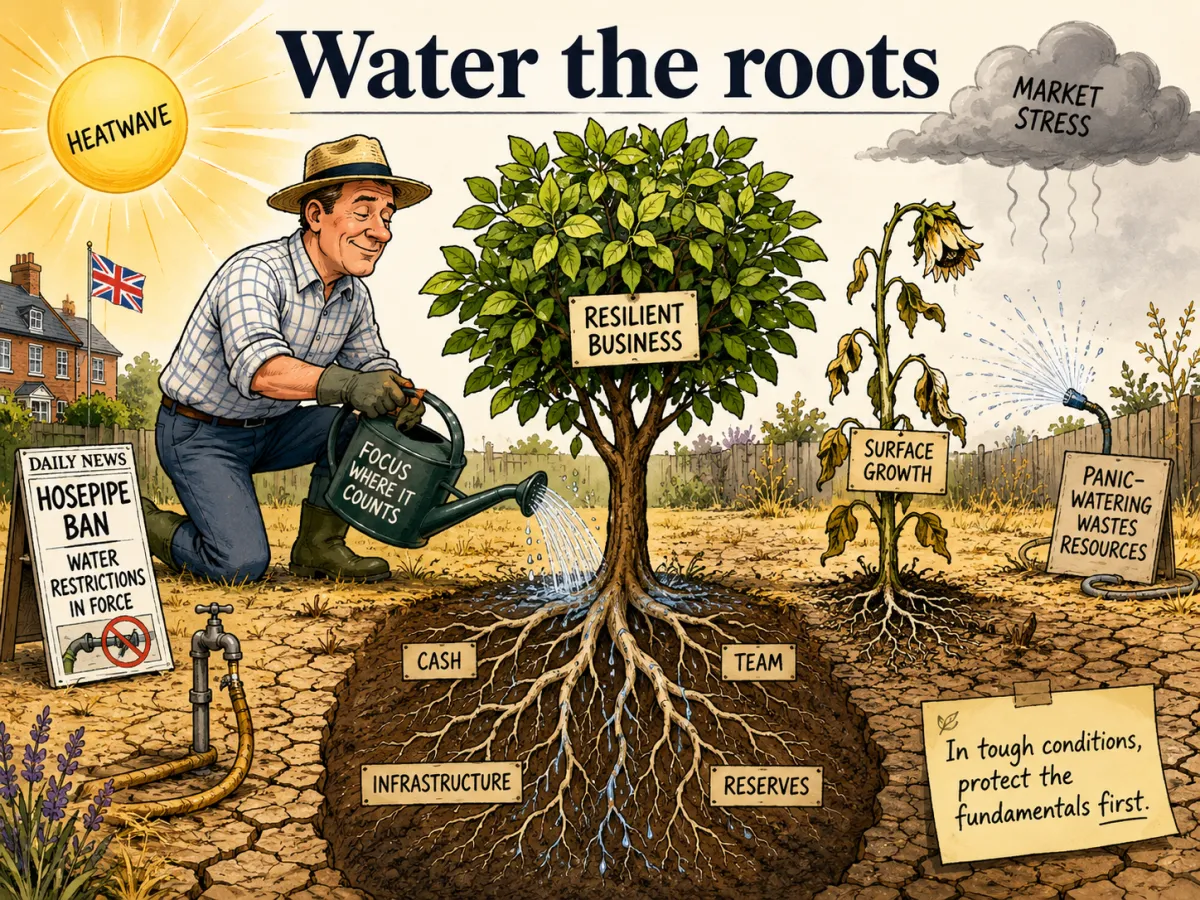

Water the roots

Britain is hot and dry this summer and, in some places, people are already being told to put the hosepipe away. Water restrictions are now part of the summer conversation again. The garden has become a small domestic version of a much bigger resource-allocation problem: when conditions get harder, you cannot keep treating water as unlimited.

The instinct in a heatwave is often to panic-water everything. That is usually the wrong move. The better approach is more selective: water early, water deeply, aim at the roots, move vulnerable pots into shade, stop feeding plants that are already stressed, and accept that the lawn may need to look ugly for a while. The point is not to keep every leaf looking perfect. The point is to keep the system alive.

There is a business lesson hiding in this. When the environment gets tougher, weak systems expose themselves quickly. Plants with shallow roots suffer first. Businesses with shallow foundations do the same. If cash is wasted on surface-level growth, if teams are stretched too thin, if infrastructure is fragile, or if management only reacts once things start wilting, the damage compounds fast.

Good operators, like good gardeners, do not wait for the heatwave to start before thinking about resilience. They build deeper roots, protect what matters, cut back what drains resources, and keep enough water in reserve for when conditions turn hostile.

The lawn can come back. Dead roots usually do not.

The Thinking Corner

When the market starts asking for proof, which companies are actually ready to show it, and which ones have only been borrowing confidence from the theme?

Latest from the team

Market commentary and field notes from the team, on The Felix View.

The securities referenced do not represent buy or sell recommendations. These notes describe corporate events and possible catalysts only. Figures are sourced from public filings, company presentations and market data; every claim links to its source. Prepared for institutional research use.